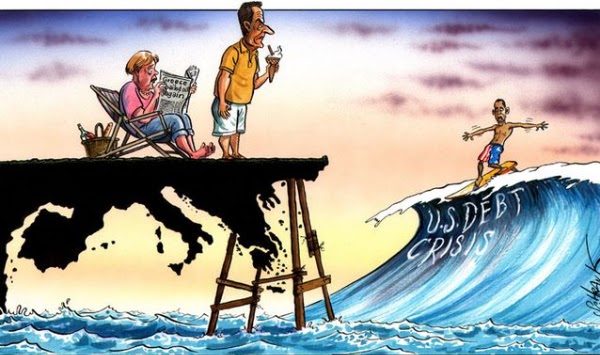

With the Greek elections between the pro-EU New Democracy party and the anti-bailout party Syriza under way, one can`t stop and think about the critical importance of today`s events. The future of the European Union may well rest on the ballets in this small Mediterranean country that accounts for only 2% of the EU combined GDP. No matter the outcome, Greek households and corporations have switched to cash, stuffing the mattresses with euro bills, just in case the economy reverts to the drachma. Greece has become in the last months a cash economy.